What is Company Formation?

Company formation refers to the legal process of establishing a new business entity in the eyes of the law. Whether you are starting a limited company, a service company, or a partnership, this process ensures that your business is officially recognized and compliant with all legal and regulatory requirements. The formation of company is essential for structuring your business properly and protecting both personal and business assets.

When a company is formed, it becomes a distinct legal entity separate from its owners. This means it can own property, enter contracts, and incur liabilities in its name. Importantly, company formation also means that the owners or shareholders are shielded from personal liability for the company’s debts, provided they do not breach any legal obligations.

In the UK, the most common type of company formation is the private limited company (Ltd), but there are various options depending on the business’s needs. The process of registering a company is handled by Companies House, which is the UK’s official company registration office.

Why Is Company Formation Important?

There are several compelling reasons why company formation is crucial for your business:

- Legal Protection: Forming a company gives you legal protection. For example, in a limited company formation, the owners (shareholders) are not personally responsible for company debts. The company’s liabilities are separate from the personal assets of the owners.

- Tax Benefits: Companies often enjoy various tax advantages. For instance, corporate taxes can sometimes be more favorable than personal income taxes. In addition, businesses can claim expenses such as salaries, office rent, and utilities to reduce their taxable profits.

- Access to Funding: Once your company is formed, you can raise funds more easily. Investors are more likely to invest in a company than in a sole proprietorship. A limited company has a clear structure and can issue shares, making it an attractive option for raising capital.

- Business Credibility: A registered company enhances your business’s credibility. Clients and suppliers are more likely to trust your business if it is a formally registered company. It shows professionalism and commitment to complying with regulations.

- Succession and Continuity: A service company or limited company can exist independently of its founders. This means that the business can continue to operate even if the original owners leave or sell their shares. This is a major advantage for long-term planning and growth.

What Are the Key Components of Company Formation?

The company formation process typically involves several key steps, including:

- Choosing the Type of Business Structure: This could be a limited company, a service company, or another type of legal entity. Your choice will depend on your business goals, tax strategy, and ownership preferences.

- Registering the Business: This includes registering with Companies House, which will issue your company a registration number and certificate of incorporation. This makes your company officially recognized by the UK government.

- Appointing Directors and Shareholders: Every company requires at least one director and one shareholder. These individuals can be the same person or different, and they are responsible for the company’s operations and financial reporting.

- Creating Legal Documents: These include the memorandum and articles of association, which outline the company’s operating procedures and governance rules. These documents are essential for any formal business structure.

- Registering for Taxes: Your business will need to be registered for various taxes, including corporation tax, VAT, and PAYE if you have employees.

The Role of Accountants in Company Formation

While it is entirely possible to complete company formation on your own, having an accountant in Slough or a chartered accountant Berkshire can make the process easier and more efficient. Accountants assist in ensuring that your company is set up correctly, helping you choose the right structure and ensuring compliance with tax regulations. Here are a few ways accountants contribute to the company formation process:

- Choosing the Right Structure: Accountants can help you decide whether a limited company formation or another structure is most suitable for your business.

- Tax Advice: They provide advice on tax-efficient structures, including guidance on capital gains tax accountants, VAT registration, and how to take advantage of any limited company tax loopholes.

- Legal Compliance: Accountants ensure that your company complies with all regulatory requirements, including submitting the correct forms to Companies House and maintaining proper records.

Key Benefits of Company Formation

- Liability Protection: One of the biggest advantages of forming a limited company is the limited liability it offers to shareholders.

- Tax Efficiency: Companies can benefit from lower tax rates, the ability to claim expenses, and various tax planning opportunities.

- Credibility and Trust: A registered company is often seen as more credible than a sole trader or partnership, which can help you build trust with customers and suppliers.

Different Types of Company Formation

When considering company formation, one of the first steps is deciding which type of company structure is best suited to your business. The choice will depend on several factors such as the size of the business, the type of services or products you provide, and the level of liability you’re willing to accept. Below, we’ll take a detailed look at the different types of company formation available in the UK.

1. Limited Company Formation (Ltd)

A limited company formation is one of the most common and preferred types of company in the UK. A limited company is a separate legal entity from its owners (shareholders). This means that the company itself can own property, enter into contracts, and be liable for its own debts. The owners are not personally responsible for business debts, except in certain circumstances such as fraud or breach of duty.

Key Benefits of Limited Company Formation:

- Limited Liability Protection: The most significant advantage is the protection it provides. The liability of the shareholders is limited to the amount they have invested in the company.

- Tax Advantages: Limited companies often benefit from a lower corporation tax rate than individuals pay on income.

- Credibility: Operating as a limited company often increases the business’s credibility in the eyes of customers, clients, and investors.

- Ownership Flexibility: Shares can be sold or transferred, and the company can continue even if a shareholder leaves or passes away.

Requirements:

- A minimum of one director and one shareholder.

- Must be registered with Companies House.

- Must file annual financial statements and tax returns.

2. Service Company Formation

A service company formation is ideal for those providing professional services, such as consultants, contractors, or freelancers. A service company is often a limited company that offers services rather than products. It could be involved in fields like accounting, legal services, IT consultancy, or any profession where the company provides a specific service to clients.

Key Benefits:

- Professional Structure: Provides a clear business structure and helps the business owner project a more professional image.

- Tax Efficiency: Allows the owner to pay themselves through a combination of salary and dividends, which can result in significant tax savings.

- Liability Protection: Like other limited companies, a service company offers limited liability, so personal assets are protected.

Requirements:

- The same as a limited company: at least one director and shareholder, registered with Companies House, and must file annual accounts.

3. New Company Formation

When starting a new company formation, you are creating a fresh entity from scratch. This process involves registering with Companies House, setting up your company structure, and complying with all legal and tax requirements. Starting a new company formation can be an exciting yet challenging process, but it is often the best option for entrepreneurs who have a new business idea that doesn’t fit within existing business structures.

Key Benefits:

- Flexibility: When setting up a new company, you have complete control over the structure and the way it operates.

- Opportunity to Build from the Ground Up: Starting fresh gives you the chance to create a business that reflects your vision, mission, and goals.

- Ownership Control: The founders have full ownership and control over the company without interference from external investors or partners.

Requirements:

- A minimum of one director and one shareholder.

- Must register with Companies House.

- Must create a Memorandum of Association and Articles of Association to define company rules.

4. Public Limited Company (PLC)

A Public Limited Company (PLC) is similar to a limited company but with one key difference: it can offer its shares to the public on the stock exchange. PLCs are typically large businesses with a wide range of shareholders. They are required to meet more stringent legal requirements, such as higher share capital.

Key Benefits:

- Access to Capital: PLCs can raise capital by offering shares to the public, which can be useful for expansion and growth.

- Enhanced Credibility: Being listed on the stock exchange enhances the company’s profile and may attract more customers, partners, and investors.

- Limited Liability: Shareholders are protected from personal liability.

Requirements:

- Minimum share capital of £50,000.

- Must have at least two directors.

- Must have at least one company secretary.

- Must comply with strict reporting and governance regulations.

5. Sole Trader

While not technically a company formation, many new business owners in the UK choose to operate as a sole trader. A sole trader is a self-employed individual who owns and operates the business. There’s no legal separation between the individual and the business, which means that the owner is personally responsible for any business debts.

Key Benefits:

- Simple Setup: Becoming a sole trader is easy and inexpensive. There are fewer legal formalities compared to other forms of company formation.

- Complete Control: The owner has full control over decision-making and business direction.

Drawbacks:

- Unlimited Liability: As a sole trader, you’re personally responsible for business debts, which puts your personal assets at risk.

- Less Credibility: Sole traders may find it more difficult to attract investors or secure business funding compared to a limited company.

- Higher Tax Rates: Sole traders pay higher income tax rates compared to the corporation tax rate paid by limited companies.

6. Limited Liability Partnership (LLP)

A Limited Liability Partnership (LLP) is a hybrid between a partnership and a limited company. It offers the flexibility of a partnership but provides the limited liability protection of a company. LLPs are often used by professionals, such as solicitors, accountants, or architects.

Key Benefits:

- Limited Liability: Partners in an LLP are not personally liable for the business’s debts beyond their capital contributions.

- Flexibility: Partners have more control over the business’s operation and management compared to a limited company.

- Tax Benefits: LLPs are not subject to corporation tax. Instead, profits are taxed at the partners’ personal income tax rates.

Requirements:

- Must have at least two members (partners).

- Must register with Companies House.

- Must file annual accounts and tax returns.

Steps to Set Up a Company

Setting up a company in the UK is a structured process that involves several key steps. From choosing your company structure to registering with Companies House, each step ensures that your business is legally compliant and set up for success. Below is a detailed guide on the steps to set up a company.

Step 1: Choose Your Company Structure

The first step in company formation is deciding which type of company best suits your needs. You can choose from several types of business structures, such as:

- Limited Company (Ltd): The most common type of company formation. It offers limited liability protection to shareholders.

- Service Company: For businesses that provide services rather than products. A service company can be a limited company that offers consulting, legal services, or IT support.

- Partnership or LLP: If you plan to run the business with others, you may consider forming a partnership or limited liability partnership (LLP).

- Sole Trader: A simpler structure where one individual owns and runs the business but does not have the liability protection of a limited company.

Choosing the right structure is important because it will affect your liability, tax obligations, and ability to raise capital. Consult with a chartered accountant Berkshire or small business accountant to help you make the right decision.

Step 2: Choose Your Company Name

Your company name is one of the first things your customers will notice, so it’s important to choose one that is memorable, relevant, and legally compliant. Here’s what to consider when choosing a name for your company:

- Unique and Available: The name must be unique and not too similar to any existing company names. You can check availability through the Companies House website.

- No Restricted Words: Some words are restricted by Companies House and may not be included in your company name unless you obtain special permission. For example, terms like “Royal” or “Bank” require prior approval.

- Descriptive and Easy to Remember: A good company name is easy to pronounce and conveys what your business is about.

Step 3: Register Your Company with Companies House

Once you have your company name and structure in place, the next step is to register with Companies House. This is the government body responsible for overseeing company formation in the UK. Registration ensures that your company is legally recognized.

What You Need for Registration:

- Company Name: As mentioned, your company name must be unique and compliant with Companies House regulations.

- Company Address: Every company in the UK must have a registered office address. This can be your business address or the address of an agent.

- Company Directors: You need to appoint at least one director for your company. Directors manage the company’s operations and ensure compliance with legal requirements.

- Shareholders: A company must have at least one shareholder. The shareholder can be the director or a separate individual or entity.

- Memorandum and Articles of Association: These documents outline the company’s governance structure and how it will be run.

Once registered, you will receive a certificate of incorporation, which confirms that your company has been officially formed.

Step 4: Open a Business Bank Account

After registering your company, the next step is to open a business bank account. A business bank account helps separate your business finances from personal finances and makes it easier to manage transactions, pay taxes, and apply for business loans.

What You Need for a Business Bank Account:

- Certificate of Incorporation: Proof that your company is legally formed.

- Proof of Identity: Identification for the company directors and shareholders.

- Company Address: The registered office address.

- Company Number: The unique company registration number issued by Companies House.

A business bank account is essential for maintaining a professional image and managing your business’s financial obligations.

Step 5: Register for Taxes

After your company is officially registered, the next step is to ensure it is properly registered for the taxes it will need to pay. Depending on your company’s size and structure, you may need to register for one or more of the following taxes:

- Corporation Tax: All UK companies must pay corporation tax on their profits. You must register with HMRC for corporation tax within three months of starting your business.

- VAT: If your taxable turnover exceeds the VAT registration threshold (£85,000), you must register for VAT. This allows you to charge VAT on sales and reclaim VAT on business purchases.

- PAYE: If you have employees, you must register for PAYE (Pay As You Earn), which is used to collect income tax and National Insurance from your employees.

- Self-Assessment: Company directors must file an annual self-assessment tax return, which includes reporting any income from the business as well as any personal income.

Step 6: Set Up Bookkeeping and Financial Systems

Proper financial management is crucial for the success of any business. As part of the company formation process, you should set up a bookkeeping system to track income, expenses, and profits. Accurate bookkeeping ensures compliance with tax obligations and provides valuable insights into your company’s financial health.

You can choose to handle bookkeeping yourself, or you can hire bookkeeping accountants or a small business accountant to ensure that your financial records are properly maintained.

Step 7: Get the Necessary Licenses and Permits

Depending on the type of business you’re running, you may need to obtain specific licenses or permits to operate legally. For example:

- Food and drink businesses may need health and safety permits.

- Construction businesses may need building permits.

- Financial services businesses will need regulatory approval from the Financial Conduct Authority (FCA).

Check with local authorities to ensure you’re compliant with all regulatory requirements for your industry.

Step 8: Set Up Payroll Services

If you plan to hire employees, you will need to set up a payroll service. This system will ensure that your employees are paid on time and that the correct tax and National Insurance contributions are deducted from their paychecks.

You can manage payroll in-house or outsource it to payroll services providers. A payroll services company can also ensure that your business complies with HMRC regulations and file the necessary reports.

Step 9: Maintain Ongoing Compliance

Once your company is set up and running, it’s essential to stay compliant with UK business regulations. Some ongoing responsibilities include:

- Annual Accounts and Returns: You must file annual accounts with Companies House and submit a company tax return to HMRC.

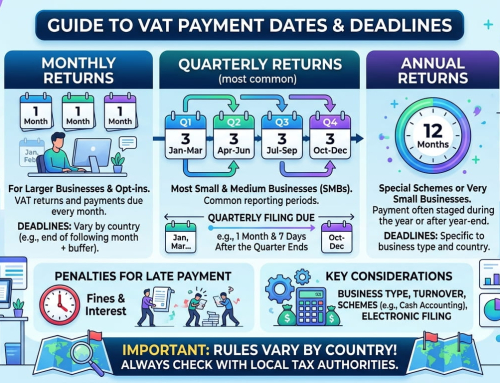

- VAT Returns: If your company is VAT-registered, you’ll need to submit quarterly or annual VAT returns.

- Paying Corporation Tax: Your company must pay corporation tax on its profits, typically within nine months of the end of its accounting period.

- Self-Assessment: Company directors must submit their self-assessment tax returns every year.

Limited Company Taxation and Benefits

One of the key reasons many business owners choose to go through the company formation process and establish a limited company is the tax advantages it offers. Understanding how limited company taxation works, as well as the associated benefits, is essential for making informed decisions about your business’s financial future. In this section, we will explore the tax obligations for limited companies and how you can maximize the financial benefits of this structure.

Corporation Tax: The Main Tax for Limited Companies

In the UK, corporation tax is the tax paid on the profits made by a limited company. Unlike sole traders and partnerships, whose income is taxed at personal income tax rates, a limited company benefits from a corporate tax rate, which is often more tax-efficient for businesses generating higher profits.

Key Points on Corporation Tax:

- Taxable Profits: A limited company is taxed on its profits, which include income from sales, investments, and other business activities, minus allowable expenses like salaries, rent, and other business costs.

- Current Rate: As of 2023, the UK corporation tax rate is 25% for businesses with profits over £250,000. For businesses with profits under £50,000, the rate is reduced to 19%. A small business accountant can help ensure you qualify for the lower rate.

- Tax Deductible Expenses: As a limited company, you can deduct a wide range of business expenses from your profits, including office rent, salaries, utilities, travel costs, and more, before calculating your corporation tax liability.

Example:

If your limited company makes a profit of £100,000 in a year, and your deductible expenses total £30,000, you will only be taxed on the remaining £70,000. At the current rate of 19%, your corporation tax liability would be £13,300.

Tax Advantages of Paying Dividends

One of the most significant benefits of forming a limited company is the ability to pay yourself in both salary and dividends. This combination can lead to significant tax savings, especially when the business is profitable.

Salary vs. Dividends

- Salary: Salaries paid to directors are subject to Income Tax and National Insurance Contributions (NICs). The salary is an allowable expense for the company, meaning it reduces the company’s taxable profits.

- Dividends: Dividends are paid out of the company’s post-tax profits, meaning they are not subject to National Insurance Contributions. They are, however, subject to Dividend Tax. The advantage is that dividend tax rates are lower than income tax rates.

Dividend Tax Rates:

- Basic Rate (up to £50,270): 8.75%

- Higher Rate (from £50,271 to £150,000): 33.75%

- Additional Rate (over £150,000): 39.35%

By taking a smaller salary and larger dividends, many limited company directors can reduce their overall tax burden. For example, if your company has £50,000 in taxable profits, and you pay yourself a £10,000 salary, the remaining £40,000 can be paid as dividends, which will be taxed at a much lower rate.

VAT Registration and Benefits

Value Added Tax (VAT) is a tax applied to the sale of goods and services. While VAT is usually associated with larger businesses, limited companies must register for VAT if their taxable turnover exceeds the current threshold of £85,000. Registering for VAT has both legal requirements and financial advantages.

Key Benefits of VAT Registration:

- Claim VAT on Purchases: If your company is VAT-registered, you can reclaim VAT on goods and services you purchase for business purposes, such as office supplies, equipment, and other business expenses.

- Better Business Image: Being VAT-registered gives your business a more professional appearance. Many larger companies and clients expect suppliers to be VAT-registered, especially for B2B transactions.

- Avoid Penalties: By registering for VAT when required, you avoid potential penalties and fines from HMRC.

How VAT Works:

When you sell goods or services, you charge VAT to your customers. If you’re VAT-registered, you then pay this VAT to HMRC after deducting the VAT you’ve paid on business expenses. This process ensures that VAT is only paid on the value added at each stage of production or service delivery.

Limited Company Tax Loopholes and Planning

One of the reasons many entrepreneurs choose limited company formations is the ability to take advantage of various tax loopholes and planning strategies that reduce the amount of tax they need to pay. Here are a few strategies commonly used by limited company owners to minimize their tax liabilities:

1. Dividend Split with Spouse

If you have a spouse or partner who is not actively involved in the business, you can consider issuing some shares to them, which would allow them to receive a portion of the dividends. This can reduce your own tax burden by spreading the dividends between two individuals.

2. Pension Contributions

Contributing to a pension scheme through your limited company is a highly tax-efficient strategy. Pension contributions are tax-deductible, meaning they reduce your company’s taxable profits and the amount of corporation tax you owe.

3. Capital Allowances

You can claim capital allowances on certain types of equipment, machinery, or assets your company purchases. This allows you to deduct the cost of these assets from your taxable profits, reducing your overall tax liability.

4. Research and Development (R&D) Tax Credits

If your business is involved in research and development activities, you may qualify for R&D tax credits. This can significantly reduce your corporation tax bill, making it an attractive benefit for businesses involved in innovation or product development.

Other Tax Benefits for Limited Companies

1. Capital Gains Tax (CGT) Relief

When selling shares in a limited company, you may be eligible for Entrepreneurs’ Relief (now known as Business Asset Disposal Relief), which offers a reduced rate of capital gains tax on the sale of business assets or shares. This relief reduces the tax rate from 20% to 10% on qualifying sales, up to a lifetime limit of £1 million.

2. Inheritance Tax Planning

As a limited company owner, you may also be able to plan for inheritance tax efficiently by transferring shares to family members. This can help minimize the impact of inheritance tax and ensure that your business remains in the family.

3. VAT on Supermarket Food UK

While most food in the UK is exempt from VAT, certain items such as hot takeaway food are subject to VAT. Understanding these VAT regulations is important for businesses in the food industry, and a VAT accountant can help you navigate these rules and avoid paying unnecessary taxes.

FAQs About Company Formation

Starting a business and going through company formation can raise many questions. Below, we have compiled some of the most frequently asked questions to provide clarity and guidance for anyone looking to set up a company in the UK.

1. What is the process of company formation in the UK?

The process of company formation in the UK involves selecting the company structure (e.g., limited company, service company), registering with Companies House, appointing company directors and shareholders, creating the Memorandum and Articles of Association, and registering for taxes like corporation tax and VAT.

2. How long does company formation take in the UK?

Once you submit your application to Companies House, the process can take as little as 24 hours if there are no issues with your registration documents. For paper applications, it may take up to 8-10 days. However, the timeline depends on the complexity of your business and whether you’re using a formation agent.

3. How much does it cost to form a company?

The cost of forming a limited company typically ranges from £12 to £100. If you use an agent for company formation services, this may incur additional fees depending on the level of service you require, such as setting up your business address, creating legal documents, or offering ongoing support.

4. Can I form a company without a physical office address?

Yes, you can form a company without a physical office address. Companies House requires a registered office address in the UK, but it doesn’t have to be your main office. Many businesses use a registered office service, which allows them to use an address for official correspondence.

5. Can I form a company without hiring an accountant?

It is not a legal requirement to hire an accountant when setting up your company. However, an accountant, such as those at Adam Accountancy, can help ensure the formation of company process is smooth, provide tax advice, assist with VAT registration, and help set up financial systems.

6. Do I need a business bank account after forming my company?

Yes, after you form your company, you should open a business bank account. It helps separate your personal and business finances, ensures compliance with tax regulations, and makes it easier to track your company’s financial transactions.

7. What taxes do I need to pay after company formation?

After forming your company, you will need to pay corporation tax on your business profits, VAT if your business turnover exceeds the VAT registration threshold, and PAYE if you have employees. Company directors are also required to file a self-assessment tax return.

8. What documents are required for company formation?

To form a company, you will need to submit the following documents:

- Memorandum of Association: A document stating that the shareholders agree to form the company.

- Articles of Association: The rules about how the company will be governed.

- Director and Shareholder Details: Information about the directors and shareholders, including their names and addresses.

- Registered Office Address: A UK address for official correspondence.

9. Can I change the name of my company after formation?

Yes, you can change the name of your company after it has been formed. You must file a resolution with Companies House and notify them of the name change. There may be a small fee for this process.

10. What is a director’s role in a limited company?

A director is responsible for managing the company’s operations, ensuring that the company complies with legal requirements, and making decisions on behalf of the company. They must ensure that taxes are paid, accounts are filed, and the business runs smoothly.

11. Can I register for VAT if my turnover is below the threshold?

Yes, you can voluntarily register for VAT even if your turnover is below the £85,000 threshold. This can be beneficial if you are in a B2B business and wish to reclaim VAT on purchases.

12. How can I claim expenses for my limited company?

As a limited company, you can claim business expenses that are wholly and exclusively for business purposes. These may include office rent, salaries, utilities, business insurance, travel, and any equipment you need to operate. These expenses can reduce your taxable profits.

13. What happens if I don’t file my company’s annual return?

Failing to file your annual return or financial statements with Companies House can result in penalties, and in the worst case, your company may be struck off the register, effectively dissolving it. Always ensure that these filings are submitted on time.

14. What is a Memorandum of Association?

The Memorandum of Association is a legal document that records the intention of the company’s members to form a company and outlines its fundamental rules. It must be signed by the initial subscribers (shareholders) at the time of registration.

15. Can I form a company with a partner?

Yes, you can form a limited company with a partner. In this case, the business is a joint venture between shareholders, and you can share responsibility for running the company. You may also choose to set up a Limited Liability Partnership (LLP), which offers similar benefits.

16. Can I use an online service to form my company?

Yes, there are many online services that offer company formation assistance. These services can help you with the paperwork, guide you through the process, and even provide additional services like virtual office addresses, legal document creation, and ongoing support.

17. How do I raise capital for my limited company?

You can raise capital for your limited company through several methods:

- Issuing shares to new investors or current shareholders.

- Taking out business loans or lines of credit from financial institutions.

- Crowdfunding or finding investors through angel networks or venture capital.

18. What is the difference between a director and a shareholder?

A director is responsible for managing the company’s day-to-day operations, while a shareholder owns part of the company through shares. Directors may or may not be shareholders, and vice versa.

19. What is a company’s Articles of Association?

The Articles of Association are a set of rules that define how the company operates and governs itself. These rules cover decision-making processes, shareholder rights, and how the company will be run. It is a legally binding document that helps resolve internal disputes.

20. How does company formation affect my personal taxes?

As a limited company owner, your salary is subject to income tax and National Insurance. However, dividends paid from company profits are subject to a lower tax rate, which can be advantageous for tax planning.

21. What is the difference between a sole trader and a limited company?

A sole trader is a business structure where the owner is personally liable for the company’s debts. In contrast, a limited company is a separate legal entity, meaning the company is responsible for its debts, not the owner.

22. Can I operate as both a director and an employee of the company?

Yes, as a director of a limited company, you can also be an employee. As an employee, you’ll receive a salary, which is subject to PAYE tax, while also being able to take dividends from the company’s profits.

23. What is the filing deadline for company accounts?

The filing deadline for company accounts is typically 9 months after the end of the company’s financial year. Failure to file on time will result in penalties.

24. Do I need an accountant to file company taxes?

While it is not a legal requirement to hire an accountant, it is highly recommended. An accountant can ensure that your taxes are filed correctly, help you with tax planning, and provide financial advice to minimize tax liabilities.

25. What is the company registration number?

The company registration number is a unique identifier issued by Companies House when your company is formed. It is used for legal and financial documentation.

26. Can my limited company trade internationally?

Yes, a limited company can trade internationally. You’ll need to comply with international trade laws, export/import regulations, and taxes, such as VAT on goods sold to other countries.

27. What is a chartered accountant’s role in company formation?

A chartered accountant Berkshire can assist with choosing the right company structure, ensuring your business complies with tax laws, advising on how to maximize tax efficiency, and handling the company’s financial records.

28. What is the role of a company secretary?

A company secretary is responsible for maintaining company records, filing annual returns, ensuring compliance with company law, and keeping the company’s governance in order.

29. Can I use a PO box as a company’s registered address?

No, Companies House does not accept PO box addresses as registered office addresses for companies. You must provide a physical address.

30. How do I ensure my company remains compliant?

Ensure your company remains compliant by filing annual accounts, paying taxes on time, keeping accurate financial records, and following any other regulations specific to your industry.

Case Studies and Examples of Successful Company Formation

Setting up a company can be daunting, but the right guidance and planning make it a smoother process. Below are case studies from different industries that highlight the benefits and challenges of company formation. These examples will provide valuable insights into the choices entrepreneurs make and how their decisions affect the long-term success of their businesses.

Case Study 1: Adam’s Digital Marketing Agency – A Limited Company Formation

Background:

Adam, a seasoned digital marketer, decided to start his own digital marketing agency. He had experience working with small businesses, helping them grow through SEO, PPC campaigns, and content marketing. After freelancing for a few years, Adam decided it was time to scale his business by forming a limited company.

Process:

Adam chose to form a limited company rather than continue as a sole trader for several reasons:

- Tax Efficiency: By incorporating as a limited company, Adam could take advantage of paying himself a smaller salary, while taking the rest of his earnings as dividends, which are taxed at a lower rate compared to regular income.

- Limited Liability: As a limited company, Adam’s personal assets would be protected from any business liabilities, a critical factor as his agency began to take on larger clients.

- Professionalism and Credibility: A limited company would give his business more credibility in the eyes of potential clients and investors. It was important for him to appear more established, which would help in attracting larger projects.

Outcome:

Adam successfully formed his company by registering with Companies House, securing his business name, and setting up the necessary legal documents. After incorporation, he opened a business bank account, registered for VAT, and hired his first employee. The company has since grown to a team of 10, with clients across the UK and internationally. The limited company structure has allowed Adam to maximize tax efficiency, protect his personal assets, and scale his agency effectively.

Lesson Learned:

Choosing a limited company structure provided the security and flexibility Adam needed to grow his business. It also ensured he could take advantage of tax-saving strategies, such as dividends and lower corporation tax rates.

Case Study 2: Bella’s Bakery – Transitioning from Sole Trader to Limited Company

Background:

Bella started her small bakery business from home as a sole trader. Initially, her sales were modest, and she ran the business part-time alongside her full-time job. However, as the demand for her baked goods grew, she realized that she needed to transition to a more formal business structure to handle the increased workload and manage business finances more effectively.

Process:

Bella decided to switch to a limited company for several reasons:

- Liability Protection: As a sole trader, Bella was personally liable for any business debts. Moving to a limited company meant that her personal assets would be protected, an important step as her business grew.

- Business Expansion: As Bella looked to expand, she needed to secure larger premises and hire employees. Forming a limited company made it easier to secure a business loan and access grants.

- Tax Efficiency: Bella’s accountant advised her that by forming a limited company, she would pay less tax overall. She could take a salary, which would be subject to personal income tax, and any additional profits could be paid out as dividends.

Outcome:

Bella successfully went through the company formation process, registered her limited company with Companies House, and received her certificate of incorporation. She secured a business loan to rent a larger bakery space and hired two full-time staff members. The tax savings from her limited company structure allowed her to reinvest in the business, expanding her product range and increasing her marketing efforts.

Lesson Learned:

Bella’s transition from a sole trader to a limited company provided the necessary legal and financial framework to grow her bakery business. The process also helped her manage her taxes better, giving her the opportunity to reinvest in the business.

Conclusion and Final Advice

In conclusion, company formation is an essential step for entrepreneurs looking to establish a legally recognized and financially sound business. Choosing the right business structure—whether it’s a limited company, service company, LLP, or another entity—plays a significant role in the long-term success of your business. It affects everything from tax obligations to liability protection and growth potential.

As we’ve seen through the case studies, each business structure has its unique advantages. For instance, forming a limited company offers the benefits of limited liability protection and potential tax advantages. Service company formation is perfect for consultants and professionals looking to operate with a tax-efficient structure, while an LLP provides the flexibility of a partnership with limited liability.

To discuss how Accountants in Slough can assist you with your Accounts Preparation, please contact us for a free, no obligation consultation on: 0333 772 1616 or complete our Contact form and we will get back to you.