Understanding your tax code is one of the most important steps you can take to manage your finances responsibly in the UK. Whether you are an employee, a self-employed professional, or a business owner, your tax code determines exactly how much income tax is deducted from your earnings. At Adam Accountancy, we specialise in making complex tax matters simple for individuals and businesses across the UK. This comprehensive guide covers the complete list of tax codes and what they mean, including HMRC updates, common errors, and expert advice to help you stay compliant and financially optimised.

What Is a Tax Code and Why Does It Matter?

A tax code is a combination of numbers and letters issued by HM Revenue and Customs (HMRC) to your employer or pension provider. It tells them how much Income Tax to deduct from your pay before it reaches your bank account.

Every employed person in the UK receives a tax code. If you have multiple jobs or pension incomes, you may have more than one tax code each applied to a different income source.

Understanding the tax code list is not just useful it is essential. An incorrect tax code can leave you paying too much or too little tax, both of which create complications. At Adam Accountancy, we regularly help clients correct tax code errors and recover overpaid tax through self-assessment and HMRC correspondence.

Why Tax Codes Change?

HMRC updates your tax code when your personal or financial circumstances change. Events that commonly trigger a change include:

- Starting or leaving a job

- Receiving company benefits such as a car or medical insurance

- Claiming Marriage Allowance or Blind Person’s Allowance

- Changes to your pension contributions

- Underpaid or overpaid tax from a previous year

- New self-employment income alongside employment

HMRC issues a PAYE Coding Notice (P2) whenever your tax code changes. It is your responsibility to check that this notice is accurate and contact HMRC if it is not.

How to Read a UK Tax Code?

The tax code uk explained process begins with understanding that most tax codes consist of a number followed by a letter for example, 1257L. The number represents your tax-free Personal Allowance divided by ten, and the letter indicates your tax situation.

So a code of 1257L means you have a tax-free allowance of £12,570, which is the standard Personal Allowance for the 2024/25 tax year. Your employer deducts tax only on income above this threshold.

However, not all tax codes follow this simple format. Some are made up of letters alone, or letters followed by numbers, indicating more specific tax circumstances. Understanding the full accounting tax codes system can seem complex, but the team at Adam Accountancy is here to simplify it for you.

Breaking Down the Components

- The Number: Represents your tax-free income divided by ten (e.g., 1257 = £12,570 allowance)

- The Letter: Indicates your personal tax situation (e.g., L = standard allowance, M = Marriage Allowance received, T = complex affairs)

- Prefixes: Codes such as K, S, C, or NT have special meanings explained in detail below

- Emergency Codes: Codes ending in W1 or M1 are emergency codes applied on a non-cumulative basis

If you are unsure what your tax code means, Adam Accountancy offers expert tax code reviews as part of our online tax services, available to clients across the UK.

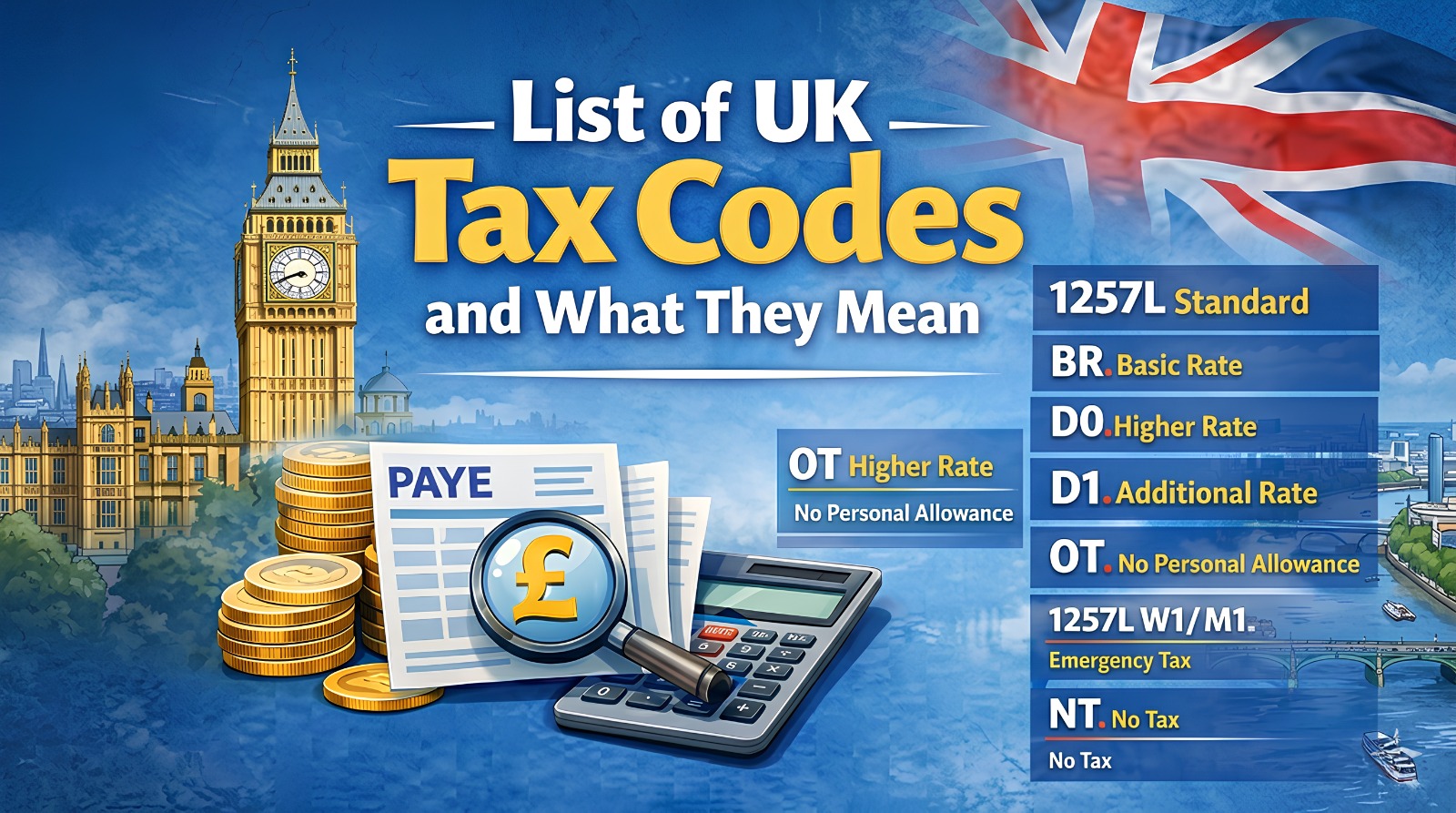

The Complete List of Tax Codes and What They Mean

Below is a detailed list of tax codes and what they mean in the UK. This is the most comprehensive hmrc tax codes list you will find, covering standard codes, prefix codes, suffix codes, and emergency codes.

Standard Numeric + Letter Codes

- 1257L — The most common tax code UK residents receive. It reflects the standard Personal Allowance of £12,570. This is applied to the majority of employees with one job and no unusual tax circumstances.

- 1257M — Applied when you have received a transfer of 10% of your partner’s Personal Allowance through the Marriage Allowance scheme. Your allowance increases to approximately £13,830.

- 1257N — The counterpart to 1257M. This is applied to the person who has transferred 10% of their Personal Allowance to their partner. Their allowance is reduced to approximately £11,310.

- BR (Basic Rate) — All income from this employment or pension is taxed at the basic rate of 20%. This typically applies when you have a second job or pension where your Personal Allowance is already used against another income.

- D0 — All income is taxed at the higher rate of 40%. Again, used when Personal Allowance is exhausted, normally on a third or additional income source.

- D1 — All income is taxed at the additional rate of 45%. Applied to very high earners with multiple income streams where their allowances are fully utilised elsewhere.

- NT (No Tax) — No tax is deducted. This can apply to individuals who are not liable for UK Income Tax, such as some contractors operating through specific structures, or in certain diplomatic situations.

K Codes — The Negative Allowance Codes

A K code is used when your tax deductions exceed your Personal Allowance. This results in a negative allowance — meaning more tax is collected each pay period. Common reasons include:

- Unpaid tax from a previous year being collected through PAYE

- High-value company benefits (such as a company car) that exceed the Personal Allowance

- State Pension or other benefits received in addition to employment income

For example, a tax code of K500 means you have £5,000 of tax liabilities that exceed your allowances. Your employer adds this to your taxable income rather than deducting it.

If you receive a K code, it is strongly advisable to seek help from a qualified chartered accountant Berkshire or other region-specific tax professional. Adam Accountancy has helped hundreds of clients understand and challenge incorrect K codes.

S Codes — Scottish Taxpayers

The prefix S indicates a Scottish taxpayer. Scotland has its own Income Tax rates and bands, which differ from the rest of the UK. Scottish taxpayers pay tax at the following rates:

- Starter Rate: 19% on income between £12,571 and £14,876

- Basic Rate: 20% on income between £14,877 and £26,561

- Intermediate Rate: 21% on income between £26,562 and £43,662

- Higher Rate: 42% on income between £43,663 and £75,000

- Advanced Rate: 45% on income between £75,001 and £125,140

- Top Rate: 48% on income above £125,140

Examples include S1257L, SBR, SD0, and SD1. The number and letter components carry the same meaning as their English counterparts, simply with the Scottish rates applied.

C Codes — Welsh Taxpayers

The prefix C is used for Welsh taxpayers. Wales currently mirrors the UK Income Tax rates, but the Welsh Government has the power to vary rates independently. Current Welsh codes include C1257L, CBR, CD0, and CD1.

The CBR tax code (also sometimes referred to as the tax code CBR) means all income from that employment is taxed at the Welsh Basic Rate. The cbr tax code functions identically to the BR code in England, with Welsh rates applied — currently 20%.

W1 and M1 — Emergency Tax Codes

These are emergency codes applied when HMRC does not have enough information to assign a standard tax code. W1 stands for Week 1 basis and M1 stands for Month 1 basis.

Under these codes, tax is calculated on a non-cumulative basis. This means each pay period is treated in isolation, and no account is taken of tax paid in previous weeks or months during the same tax year.

- W1/M1 appended to a standard code: e.g., 1257L W1 or 1257L M1

- These are temporary codes — HMRC will usually correct them once they have the right information

- If you remain on an emergency code for more than one or two pay periods, contact HMRC or speak to Adam Accountancy

OT Code

The OT code means your Personal Allowance has been completely used up or that you have started a new job and your employer does not yet have your P45 details.

Under the OT code, you receive no tax-free pay. Tax is deducted at the relevant marginal rates. This code can result in an overpayment of tax, which you can reclaim at the end of the tax year via self-assessment or by contacting HMRC.

T and 0T Codes

A T code is used when your tax affairs are too complex for a standard code — for example, if you are a company director or have multiple sources of income. The T code indicates that HMRC needs to review your situation personally.

0T (zero T) is used when all allowances have been exhausted, and you have no free pay at all. Tax is deducted at the marginal rate on all earnings. This is different from OT — the zero indicates a zero allowance figure.

Types of Tax Code: A Breakdown by Purpose

Understanding the various types of tax code helps you identify why you have been assigned a specific code and what it means for your take-home pay. Here is a summary of the main type of tax code categories:

- Personal Allowance Codes: These reflect your tax-free income entitlement. The most common example is 1257L.

- Nil Tax Codes: Codes like NT mean no tax is deducted at all.

- Flat Rate Codes: BR, D0, D1 apply a fixed rate to all earnings from that source, with no allowance.

- Negative Allowance Codes: K codes increase the amount of taxable income rather than reducing it.

- Emergency Codes: W1 and M1 are temporary, non-cumulative codes pending further HMRC information.

- Special Situation Codes: T and OT codes indicate complex or unusual circumstances.

- Regional Codes: S (Scottish) and C (Welsh) codes apply the respective devolved Income Tax rates.

- Non-Standard Codes: Codes such as NT or specific codes for non-residents and diplomats.

Adam Accountancy provides specialist advice on all of these categories. Whether you are a sole trader, a company director, or an individual employee, our team of experienced accounting tax codes specialists can review your position and ensure you are paying the right amount of tax.

The Most Common Tax Code UK Workers Receive

The most common tax code UK workers are assigned is 1257L. For the 2024/25 tax year, this reflects the Personal Allowance of £12,570, which is the amount you can earn before Income Tax applies.

According to HMRC data, the majority of UK employees are on the 1257L tax code. If you are on this code and have a single employment income, you should be paying the correct rate of tax automatically through the PAYE system.

However, even those on 1257L should periodically review their tax position. Changes to benefits, pension contributions, or additional income can affect how much tax you should be paying. Adam Accountancy offers annual tax health checks to give you peace of mind.

Other Frequently Used Codes

- BR — Very common among people with a second job or pension. All income from that source is taxed at 20%.

- D0 — Used for high earners with multiple incomes. A higher rate of 40% is applied.

- K codes — More common than many people realise, particularly among those receiving company benefits or who have underpaid tax in previous years.

- S1257L — The Scottish equivalent of 1257L; the most common code in Scotland.

- OT — Frequently seen at the start of a new employment when a P45 is not available.

Understanding the HMRC Tax Codes List and How HMRC Assigns Codes

The list of tax codes and what they mean hmrc publishes officially is available on the GOV.UK website. HMRC assigns and updates tax codes based on information they receive from:

- Your employer (via Real Time Information / RTI submissions)

- Previous tax returns and self-assessment forms

- Benefits in Kind (P11D forms) submitted by employers

- Information from the DWP regarding State Pension or other taxable benefits

- Changes you notify HMRC about directly via your personal tax account HMRC portal

Your personal tax account hmrc is an online portal where you can check your current tax code, see your annual tax summary, update your personal details, and claim certain allowances. Adam Accountancy strongly encourages all clients to set up and regularly check their personal tax account.

How HMRC Communicates Code Changes

- A P2 Notice of Coding is issued by HMRC when your code changes

- Your payslip will show your current tax code — check it every month

- Your employer receives a tax code notice directly from HMRC via the PAYE system

- You can also check and query your tax code by calling HMRC or through your personal tax account

If you believe your tax code is wrong, do not wait. Contact HMRC directly or seek advice from a professional. Adam Accountancy handles HMRC correspondence on behalf of clients, making the process stress-free.

Tax Codes for Specific Employment Situations

Different employment situations attract different tax codes. Below is a guide to some of the most common scenarios our clients at Adam Accountancy encounter.

Second Jobs and Multiple Employments

When you have more than one job, your Personal Allowance is typically allocated entirely to your primary employment. Your second or subsequent jobs will usually carry one of the flat-rate codes:

- BR: 20% basic rate applied to all earnings from that job

- D0: 40% higher rate applied — used if your combined income exceeds the higher rate threshold

- D1: 45% additional rate — for very high earners

It is essential to ensure the allocation of your Personal Allowance is correct. If your main job does not pay enough to fully use the allowance, you may wish to split it between employers. Contact Adam Accountancy or HMRC to request a reallocation.

Pension Income

Retirees receiving one or more pensions may have different tax codes applied to each pension. The primary pension usually carries a standard code such as 1257L, while additional pensions are taxed at BR or D0.

State Pension is taxable but is paid without any tax deduction at source. HMRC adjusts your other tax codes to collect the tax owed on the State Pension — which is why your tax code on your private pension may be lower than expected.

Self-Employment Alongside PAYE

Many people in the UK have a combination of employed and self-employed income. If this applies to you, HMRC may adjust your PAYE tax code to collect tax owed on your self-employed profits, reducing the need for a large self-assessment accountant payment at year end.

However, this system is not always perfectly accurate. A qualified self-assessment accountant at Adam Accountancy can review your situation and ensure you are not being over or under-taxed through your PAYE code.

Company Directors

Company directors often have complex tax affairs involving salary, dividends, and benefits in kind. A corporation tax accountants team like ours at Adam Accountancy can help directors manage their tax codes alongside their corporate tax obligations effectively.

Directors may receive T codes or have their allowances reduced due to high earnings, benefits-in-kind, or dividend income. It is vital to review your tax code annually if you are a director.

Landlords and Property Income

If you are a landlord, your rental income may be coded into your PAYE code through an adjustment, particularly if you prefer to avoid submitting a self-assessment return. Landlord accountants at Adam Accountancy regularly advise clients on the best way to handle rental income, including whether PAYE coding is the most efficient approach.

Landlords with significant rental portfolios often benefit from dedicated property tax advice to ensure they are claiming all available reliefs and structuring their affairs correctly.

VAT Tax Codes and How They Differ from Income Tax Codes

While this guide primarily focuses on Income Tax codes, it is worth briefly explaining vat tax codes — a separate coding system used for Value Added Tax purposes, often important for businesses and their accounting software.

VAT tax codes are used within accounting systems (such as Xero, QuickBooks, or Sage) to categorise transactions according to the applicable VAT treatment. They help businesses accurately calculate VAT returns and are distinct from PAYE tax codes.

Common VAT Tax Code Categories in Accounting Software

- T0 or Z: Zero-rated VAT — goods and services taxed at 0% (e.g., most food, children’s clothing, books)

- T1 or S: Standard rate VAT — currently 20% in the UK

- T2 or E: Exempt from VAT — such as financial services, insurance, and some medical services

- T9 or O: Outside the scope of VAT — such as internal transactions and payroll costs

- T4 or RC: Reverse charge VAT — used for specific business-to-business transactions

Understanding vat on supermarket food uk is a good practical example: most basic foodstuffs are zero-rated for VAT, but items such as crisps, confectionery, and alcoholic drinks are standard-rated at 20%.

A specialist VAT accountant at Adam Accountancy can ensure your business is applying the correct VAT tax codes, avoiding costly errors or HMRC penalties.

Service Tax Code Explained

The service tax code and code of service tax are terms sometimes used in reference to the categorisation of service-related transactions for VAT purposes. In UK accounting software, services provided by UK-registered businesses to UK customers are typically coded at the standard VAT rate of 20%, unless specifically exempt or zero-rated.

For businesses providing services internationally, the VAT treatment varies depending on whether the customer is a business or a consumer, and their country of residence. Adam Accountancy’s VAT accountant team can guide you through the complexities of service VAT coding.

Tax Codes for Specific Business Structures

The type of business structure you operate under can have a significant impact on your tax code and overall tax position. Here is a summary of how different structures are affected.

Sole Traders

Sole traders are self-employed individuals who pay Income Tax and National Insurance through the self-assessment system. They do not typically receive a PAYE tax code unless they also have employed income.

A small business accountant at Adam Accountancy can help sole traders file their self-assessment tax return accurately, maximising allowable expenses and minimising their tax bill.

Partnerships

Partners in a business partnership are each treated as self-employed for tax purposes. Each partner receives their own share of profits and is responsible for reporting this via self-assessment. The partnership itself does not pay Income Tax.

VAT may apply to the partnership depending on turnover, and our bookkeeping accountants can manage the VAT registration and returns process on your behalf.

Limited Companies

Directors and shareholders of limited companies are taxed differently from employed individuals. The company pays Corporation Tax on profits, while directors receive a salary (coded through PAYE) and often take dividends, which are not subject to National Insurance.

Utilising limited company tax loopholes — or more accurately, legally available tax-saving strategies — can significantly reduce a director’s overall tax burden. Adam Accountancy’s corporation tax accountants are experts in this area.

CIS (Construction Industry Scheme)

Subcontractors operating under the Construction Industry Scheme receive income with tax deducted at source by the contractor. The standard CIS deduction rate is 20% for registered subcontractors and 30% for those not registered with HMRC.

CIS deductions are credited against the subcontractor’s total tax liability when they file their self-assessment return. Adam Accountancy handles CIS returns for many clients in the construction sector.

UK Tax Code List for Non-Residents and Special Cases

The uk tax code list includes some codes that apply specifically to non-residents, expats, or individuals with unusual employment arrangements. Below are some of the less common but important codes you should know.

NT Code — No Tax

As mentioned earlier, the NT code means no tax is deducted. This is sometimes used for:

- Non-UK residents who are not subject to UK Income Tax

- Diplomats and certain foreign government employees

- Individuals who have been confirmed as having no UK tax liability

- Some specific contractor arrangements reviewed and approved by HMRC

X Code

The X code is rare and used when HMRC cannot determine the correct tax treatment. It may appear on an emergency basis while investigations or reviews are ongoing. Tax is calculated as if the code were OT in many systems.

Codes for Seafarers and Offshore Workers

Seafarers who qualify for Seafarers’ Earnings Deduction (SED) may have an adjusted tax code reflecting the 100% deduction available on qualifying earnings. This is a specialist area, and our team at Adam Accountancy can advise those working in the maritime industry.

Codes for Individuals with Blind Person’s Allowance

Individuals registered as blind or severely sight-impaired are entitled to the Blind Person’s Allowance. For 2024/25, this is £3,070 in addition to the standard Personal Allowance. This is reflected in an upward adjustment to the numeric portion of the tax code.

List of UK Tax Codes: Summary Table

For quick reference, here is a comprehensive list of uk tax codes and their meanings:

- 1257L — Standard allowance (£12,570), one employer, no complications

- 1257M — Received Marriage Allowance from partner

- 1257N — Transferred Marriage Allowance to partner

- BR — Basic Rate (20%) on all income from this source

- D0 — Higher Rate (40%) on all income from this source

- D1 — Additional Rate (45%) on all income from this source

- NT — No tax deducted

- K[number] — Negative allowance; income is increased for tax purposes

- S[code] — Scottish taxpayer rates apply

- C[code] — Welsh taxpayer rates apply

- CBR / tax code CBR — Welsh Basic Rate (20%) on all income from this source

- [code]W1 or [code]M1 — Emergency code; Week 1 or Month 1 basis (non-cumulative)

- OT — No allowances; tax at marginal rates

- T — Complex affairs; HMRC will review individually

- 0T — Zero allowance; all income taxed at marginal rates

This tax codes list is accurate for the 2024/25 tax year. Tax codes can change annually as the Personal Allowance and tax thresholds are reviewed by the government.

Common Tax Code Errors and How to Fix Them

Even with the best systems in place, errors in common tax codes do occur. Here are the most frequent mistakes and what to do about them.

You Are on an Emergency Code

If you start a new job and your employer does not have your P45, you may be put on an emergency code such as 1257L W1/M1 or OT. This means your tax is not being calculated cumulatively.

To fix this, provide your employer with your P45 or contact HMRC to confirm your correct code. Adam Accountancy can liaise with HMRC on your behalf to get this resolved quickly.

Your Personal Allowance Is Wrong

If HMRC has incorrect information about your benefits, pension, or other income, they may have reduced your Personal Allowance incorrectly. Review your P2 Coding Notice carefully.

Common reasons for a reduced allowance include outstanding tax debts, underpaid tax from previous years, or benefits in kind that HMRC has overestimated. Check with your employer that the benefits values they have reported are accurate.

You Have Not Claimed All Available Allowances

- Marriage Allowance — worth up to £252 per year

- Blind Person’s Allowance — worth up to £3,070 per year

- Maintenance Payments Relief — for those paying maintenance under a court order

- Professional Subscriptions — claimable as a deduction via PAYE adjustment

Adam Accountancy’s team regularly identifies unclaimed allowances for clients, resulting in significant tax savings and refunds.

Your Tax Code Has Not Been Updated After a Life Event

Marriage, divorce, a change in employment, retirement, or receiving an inheritance can all affect your tax position. If HMRC is not updated promptly, your tax code may become inaccurate.

For those receiving an inheritance, it is worth understanding your potential liability and speaking with an inheritance tax advisor at Adam Accountancy to ensure proper planning.

How Tax Codes Relate to Payroll and PAYE?

From an employer’s perspective, tax codes are the cornerstone of the PAYE (Pay As You Earn) system. Getting tax codes right is a fundamental part of running compliant payroll services.

Adam Accountancy provides full payroll services to businesses of all sizes, ensuring that PAYE deductions are calculated correctly and submitted to HMRC on time. Our payroll team handles:

- Processing weekly and monthly payroll runs

- Applying the correct tax codes from HMRC notifications

- Submitting RTI (Real Time Information) returns to HMRC

- Managing year-end P60 and P11D submissions

- Handling starters, leavers, and code changes

- Dealing with HMRC queries and payroll audits

Errors in payroll tax codes can result in HMRC penalties, unhappy employees, and complicated year-end adjustments. Outsourcing your payroll to an experienced team such as Adam Accountancy eliminates this risk.

Employer Responsibilities

- Always apply the tax code shown on the HMRC P6 or P9 coding notice immediately

- If you receive conflicting information, contact HMRC before making any changes

- Never assume a tax code — always verify through HMRC’s online systems

- Ensure new starters complete a starter checklist if a P45 is not available

- Report any changes to employees’ circumstances that may affect their tax code via RTI

Tax Codes and Capital Gains Tax

Capital Gains Tax (CGT) is not collected via PAYE and therefore does not directly affect your PAYE tax code. However, there is an important indirect relationship.

If you have underpaid Capital Gains Tax in a previous year and HMRC cannot collect it through a CGT payment, they may in limited circumstances adjust your PAYE code to collect smaller amounts. For larger CGT liabilities, self-assessment is always required.

Adam Accountancy’s team of capital gains tax accountants advises individuals and businesses on all aspects of CGT, including property disposals, business asset sales, shares and investments, and how to maximise your Annual Exempt Amount.

If you have sold a property, business, or significant investment, it is essential to review your Capital Gains position with a specialist before the end of the tax year.

Stamp Duty and Equity Transfers

While not directly related to tax codes, many clients of Adam Accountancy ask about stamp duty on transfer of equity and stamp duty on a transfer of equity in the context of property transactions. A transfer of equity occurs when someone is added to or removed from a property title.

Stamp Duty Land Tax (SDLT) on a transfer of equity depends on whether any consideration (money or debt) changes hands. If a mortgage is involved, SDLT may apply on the share of the mortgage assumed by the new owner. Adam Accountancy’s property tax advice service covers SDLT in detail.

Inheritance Tax and Tax Codes

Inheritance Tax (IHT) does not affect your PAYE tax code directly, as it is a one-off charge on the estate of a deceased person. However, understanding your IHT position is an important part of overall tax planning.

If you need to complete an inheritance tax summary form (IHT205 or the newer IHT400 series), Adam Accountancy’s inheritance tax advisor team can guide you through the process and ensure all available reliefs and exemptions — including the Residence Nil Rate Band — are claimed.

The current IHT threshold (nil rate band) is £325,000 per person, with an additional residence nil rate band of £175,000 for those leaving a home to direct descendants. Proper planning can significantly reduce the IHT liability on your estate.

Charity and Not-for-Profit Tax Codes

Charities have a unique tax position. Registered charities are generally exempt from Income Tax, Corporation Tax, and Capital Gains Tax on income and gains applied to charitable purposes. Charity accountants at Adam Accountancy specialise in this sector.

Gift Aid is a key benefit for charities — donations made by UK taxpayers allow the charity to reclaim basic rate tax (20%) on the donation, effectively increasing its value by 25%. Higher-rate taxpayers can also claim additional relief through their own self-assessment.

From a payroll and PAYE perspective, charity employees are subject to the same tax code rules as any other employee. However, specific Gift Aid payroll giving schemes allow employees to donate directly from gross pay, reducing their taxable income before tax codes are applied.

International Considerations and Forex

For UK residents earning income in foreign currencies, tax codes can become particularly complex. HMRC requires that all foreign income is reported in sterling, using the exchange rate at the time of receipt.

A specialist forex accountant uk at Adam Accountancy can assist those with income from overseas employment, foreign investments, cryptocurrency, or other foreign-denominated assets. Accurate reporting of foreign income is essential to maintain the correct PAYE tax code and avoid HMRC penalties.

Non-domiciled individuals living in the UK face additional complexity around the remittance basis of taxation. Our team has significant experience advising non-doms on how their residency status interacts with their UK tax code and overall liability.

How Adam Accountancy Can Help You?

At Adam Accountancy, we are committed to providing expert, approachable, and affordable tax and accounting services to individuals and businesses across the UK. Whether you are searching for accountants in slough, accountants slough, or a nationwide provider of online tax accountants, Adam Accountancy has the expertise and digital tools to serve you wherever you are.

Our Services Include

- Tax code reviews and HMRC correspondence

- Self-assessment tax returns and tax planning

- Corporation tax returns for limited companies

- VAT registration, returns, and advisory services

- Full payroll and bookkeeping services

- Capital gains, inheritance tax, and property tax advice

- Chartered accountant services across Berkshire and beyond

- Online tax services available to clients throughout the UK

- Specialist advice for landlords, charities, forex traders, and non-doms

Whether you need a chartered accountant Berkshire for a local face-to-face meeting, or prefer the flexibility of our online tax services, we offer both. Our bookkeeping accountants keep your records accurate and up to date, while our tax specialists focus on maximising your savings and ensuring compliance.

Frequently Asked Questions (FAQs) About Tax Codes

Q1. What is the most common tax code in the UK?

The most common tax code UK employees receive is 1257L. This reflects the standard Personal Allowance of £12,570 for the 2024/25 tax year. Most full-time employees with one job and no unusual circumstances will be on this code.

Q2. What does BR mean on my tax code?

BR stands for Basic Rate. It means all income from that employment or pension is taxed at 20% with no Personal Allowance applied. This code is commonly used on second jobs or additional pensions where your Personal Allowance is already being used elsewhere.

Q3. Why do I have a K tax code?

A K code means you have tax liabilities that exceed your Personal Allowance. This often happens when you have underpaid tax from previous years, receive company benefits that are worth more than your allowance, or receive State Pension or other taxable benefits alongside employment income. Contact HMRC or speak to Adam Accountancy if you are unsure why you have a K code.

Q4. What is an emergency tax code?

An emergency tax code such as 1257L W1 or 1257L M1 is applied when HMRC does not have enough information to assign a standard code. The W1 (Week 1) and M1 (Month 1) suffixes mean tax is calculated on a non-cumulative basis. These are temporary and should be corrected once HMRC receives the necessary information.

Q5. What does the CBR tax code mean?

The CBR tax code applies to Welsh taxpayers and means all income from that source is taxed at the Welsh Basic Rate, which is currently 20%. It functions similarly to the standard BR code but with Welsh Income Tax rates applied. The tax code CBR is assigned by HMRC based on the address on your records.

Q6. How do I check my tax code?

You can check your tax code on your payslip, your P60 at the end of the tax year, any HMRC P2 Coding Notice you have received, or by logging in to your personal tax account HMRC portal at gov.uk. You can also contact HMRC directly by phone or have Adam Accountancy check it on your behalf.

Q7. Can I have different tax codes for different jobs?

Yes. If you have more than one job or income source, each one can have a different tax code. Your Personal Allowance is usually allocated to your main employment, and additional jobs typically receive a BR or D0 code. It is possible to split your allowance between employers if appropriate.

Q8. What is the difference between OT and 0T?

OT (letter O, letter T) means your Personal Allowance has been used up or you started a new job without a P45. 0T (zero, letter T) means you have a zero allowance all income is taxed at marginal rates. They function very similarly but arise from slightly different circumstances.

Q9. How does the S code apply to Scottish taxpayers?

Scottish taxpayers pay Income Tax at different rates than those in England, Wales, and Northern Ireland. The S prefix on your tax code (e.g., S1257L) tells your employer to apply Scottish Income Tax rates and bands rather than the UK standard rates. HMRC assigns this based on your home address in Scotland.

Q10. What should I do if I think my tax code is wrong?

If you believe your tax code is incorrect, you should contact HMRC directly using the information on your P2 Coding Notice, or log in to your personal tax account to review and update your details. Alternatively, Adam Accountancy can handle HMRC correspondence on your behalf and ensure any errors are corrected promptly and any overpaid tax is refunded.

Q11. What does the accounting tax codes system mean for businesses?

For businesses, accounting tax codes serve two purposes. In payroll, they determine how much Income Tax to deduct from employees’ wages under PAYE. In accounting software, VAT tax codes categorise transactions for VAT return purposes. Both types must be managed accurately to remain compliant with HMRC. Adam Accountancy’s bookkeeping accountants and payroll team handle both.

Q12. Can my tax code affect my self-assessment?

Yes. If HMRC has adjusted your tax code to collect additional tax (for example, from self-employment profits or rental income), this affects how much you owe or are owed at the end of the tax year via self-assessment. A qualified self assessment accountant can ensure these interactions are correctly accounted for in your annual return.

About Adam Accountancy

Adam Accountancy is a leading UK-based firm of qualified accountants and tax advisers providing comprehensive financial services to individuals, small businesses, and corporate clients. Our areas of expertise include:

- Chartered accountant Berkshire and wider South East England services

- Small business accountant support for sole traders, partnerships, and limited companies

- Self-assessment accountant services for individuals with complex tax affairs

- Corporation tax accountants for UK limited companies and groups

- VAT accountant and compliance services

- Bookkeeping accountants for real-time financial management

- Payroll services for businesses of all sizes

- Landlord accountants and property tax advice specialists

- Capital gains tax accountants for property and investment disposals

- Inheritance tax advisor services for estate and succession planning

- Charity accountants for not-for-profit organisations

- Online tax accountants serving clients throughout the UK

- Forex accountant UK services for those with overseas income

At Adam Accountancy, we believe great tax advice should be accessible to everyone. Whether you are searching for accountants slough, need a VAT accountant for your business, or are looking for expert guidance on stamp duty on transfer of equity, we have the expertise and dedication to deliver exceptional results.

Get in touch with Adam Accountancy today and let us take the complexity out of your tax affairs so you can focus on what matters most.

To discuss how Accountants in Slough can assist you with your Accounts Preparation, please contact us for a free, no obligation consultation on: 0333 772 1616 or complete our Contact form and we will get back to you.