If you run a limited company, UK corporation tax thresholds shape how much tax you pay, when you pay it, and how you plan profit extraction.

In this guide for a UK audience, Adam Accountancy explains the corporation tax thresholds uk for 2026, how Marginal Relief works, and what to watch when you move from tax threshold 2025 to 2026.

You’ll also see practical case studies, checklists, and FAQs—written to help you make confident decisions around tax thresholds 2026.

What “Corporation Tax Thresholds” Actually Means

In everyday language, “thresholds” usually means “the point where something changes”.

For Corporation Tax, thresholds can affect:

- Which rate applies to your profits

- Whether Marginal Relief applies

- Whether you must pay in instalments

- How group/associated company rules reduce limits

So when people search “tax threshold 2026”, they’re often asking: Where are the profit bands in 2026—and what changes when I cross them?

UK Corporation Tax Thresholds 2026: The Key Numbers

For the financial year starting 1 April 2026, the UK continues with the same headline structure:

- Small profits rate: 19% (profits up to £50,000)

- Main rate: 25% (profits above £250,000)

- Marginal Relief band: profits between £50,000 and £250,000 (effective marginal rate can be higher than 25%)

These are the core uk corporation tax thresholds most companies care about.

Important nuance: the thresholds can be reduced if you have associated companies or a short accounting period.

Image Ideas You Can Add to the Article

Image idea 1 (infographic): “Corporation Tax bands for 2026 (19% / Marginal Relief / 25%)”

Alt text: uk corporation tax thresholds 2026 bands explained

Source reference: GOV.UK rates and allowances table.

Image idea 2 (flowchart): “Do I qualify for Marginal Relief?”

Alt text: corporation tax thresholds uk marginal relief flowchart

Source reference: GOV.UK Marginal Relief guidance.

Image idea 3 (timeline graphic): “Payment vs filing deadlines”

Alt text: corporation tax payment deadline 9 months and 1 day UK

Source reference: GOV.UK payment and return deadlines.

How Marginal Relief Works in 2026 (Plain English)

If your profits land in the middle band, you start at the 25% main rate, then reduce the bill using Marginal Relief.

That sounds friendly, but there’s a catch.

Because of how the calculation works, profits in this band can face an effective marginal rate of 26.5% on the “slice” of profit in the band.

What this means in practice:

As profits rise from £50k to £250k, your overall effective rate rises gradually from 19% toward 25—but the extra profit in that zone is often taxed more harshly.

Marginal Relief: A Worked Example (2026)

Let’s assume a single company (no associates), 12-month accounting period.

Example: taxable profits = £100,000

A simple illustration (based on the standard Marginal Relief approach):

- Tax at main rate: £100,000 × 25% = £25,000

- Less Marginal Relief (per HMRC-style example workings): £2,250

- Corporation Tax due: £22,750

This is why “just multiply by 25%” is rarely accurate in the middle band.

Associated Companies: The Threshold Trap Many Owners Miss

From April 2023 onwards, the lower and upper limits are divided by the total number of associated companies + 1 (i.e., your company plus its associates).

So if you have three associated companies, you don’t keep £50k and £250k.

You get:

- Lower limit: £12,500 (£50,000 ÷ 4)

- Upper limit: £62,500 (£250,000 ÷ 4)

That can push small groups into the 25% regime far earlier than expected.

Common situations that create “associates”:

- A founder sets up separate companies for different activities

- A family owns multiple trading companies

- A group structure exists for property vs trading

- A “newco” is created for a side venture

Short Accounting Periods Also Reduce Thresholds

If your accounting period is less than 12 months, the thresholds are pro-rated.

That’s especially relevant if:

- you’ve just incorporated

- you change your year-end

- you have accounts longer than 12 months (often split into separate Corporation Tax periods)

In those situations, you can end up with two returns and adjusted thresholds to match the tax periods.

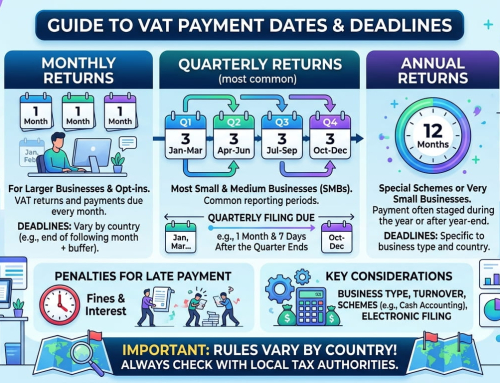

The Instalment Payments Threshold: When “Big Company” Rules Start

Another key part of corporation tax thresholds uk is how you pay.

If taxable profits are up to £1.5 million, most companies pay Corporation Tax 9 months and 1 day after the accounting period ends.

If your company is “large”, you may need to pay Corporation Tax in quarterly instalments.

HMRC’s instalment regime applies when annual taxable profits are between £1.5 million and £20 million (with “very large” rules above that).

Note: in groups, that £1.5m limit can be divided across related companies, making instalments relevant sooner than expected.

Filing Deadlines vs Payment Deadlines (Don’t Mix Them Up)

Two deadlines matter every year:

- Pay your Corporation Tax: usually 9 months and 1 day after your accounting period ends

- File your Company Tax Return (CT600): 12 months after the end of the accounting period

This is a classic cashflow mistake: businesses file “on time” but pay “late”.

Planning Tips Around UK Corporation Tax Thresholds 2026

Good planning is less about “avoiding tax” and more about timing, structure, and documenting decisions.

Here are practical actions many SMEs consider around tax thresholds 2026.

Quick wins (often immediate impact)

- Forecast profits quarterly, not once a year

- Check associated company status before assuming you have the full thresholds

- Budget for instalments if you’re approaching £1.5m profits

- Track “augmented profits” concepts where relevant for Marginal Relief calculations

Operational planning (business-led decisions)

- Bring forward essential spending where it genuinely supports growth

- Review pricing and margins if you’re stuck in the Marginal Relief band

- Consider year-end timing (not to game tax, but to smooth cashflow and admin)

- Clean up intercompany arrangements if you have multiple entities

Owner-manager strategies (needs tailored advice)

- Salary vs dividends strategy (must match your broader tax position)

- Pension contributions (company vs personal)

- Group simplification (only where commercially sensible)

- Succession planning (ties into IHT and shareholder planning)

Case Study 1: Small Consultancy Under the Lower Threshold

Scenario: A one-director consultancy forecasts £45,000 taxable profits in FY 2026.

Outcome:

This sits within the £50,000 small profits band, so the company is generally within the 19% small profits rate zone.

Planning takeaways:

- Keep an eye on late invoices or project overruns that push profits over £50k

- Don’t assume the full threshold applies if a second company exists in the background

- Budget for Corporation Tax payment date (9 months + 1 day)

Case Study 2: Growing E-commerce Business in Marginal Relief

Scenario: An online retailer forecasts £140,000 taxable profits.

Outcome:

Profits sit between £50k and £250k, so Marginal Relief should apply (subject to conditions), and the business may face an effective marginal rate on the band that feels higher than expected.

Planning takeaways:

- Model profit scenarios: £120k vs £160k can produce surprises

- Consider cashflow: tax due may rise faster than profit

- Use forecasting to decide when to reinvest vs distribute

Case Study 3: Two Companies, One Owner—Thresholds Halved

Scenario: A trades business forms a second company for a new division. Both are under common control.

Outcome:

If they are treated as associated companies, thresholds can be divided, reducing the Marginal Relief band dramatically.

Planning takeaways:

- Build structures for commercial reasons, not just “neatness”

- Get advice before adding another company, especially where profits are rising

- Avoid accidental complexity that increases admin and tax risk

Case Study 4: Approaching £1.5m—Instalments Become a Cashflow Event

Scenario: A tech services firm scales rapidly and forecasts £1.7m taxable profits.

Outcome:

The company may fall into the quarterly instalment payment regime for large companies.

Planning takeaways:

- Instalments can change the cashflow profile quickly

- Don’t wait for the year-end to plan—forecast tax during the year

- Groups should confirm whether the £1.5m limit is effectively reduced

Tax Threshold 2025 to 2026: What Actually Changes?

For many companies, the headline Corporation Tax structure is stable as you move from tax threshold 2025 to 2026.

GOV.UK’s rate structure (19% / Marginal Relief / 25%) remains the framework, and legislation confirms the main rate and small profits rate for FY 2026. Where businesses often feel “change” is in:

- profit growth pushing them into different bands

- associated companies reducing thresholds

- payment method changing (instalments)

- wider tax changes influencing extraction decisions (dividends, savings, etc.)

So the practical shift from 2025 to 2026 is often your numbers—not the rates.

Inheritance Tax Threshold Freeze Implications 2026 (For Business Owners)

This guide is about Corporation Tax, but directors and shareholders often plan across taxes.

By 2026, the Inheritance Tax nil-rate band is still a major planning factor, and policy changes have been widely reported.

Key points commonly referenced for planning:

- Nil-rate band of £325,000 and residence nil-rate band £175,000 remain central reference points in official policy discussions. Public reporting has discussed extending threshold freezes further and introducing reforms affecting business and agricultural reliefs from April 2026, plus pensions from April 2027. Why this matters alongside corporation tax thresholds uk:

- Shares in trading companies can be part of an estate

- Group structures can complicate valuation and relief eligibility

- Dividend strategies can affect personal wealth accumulation

- Succession planning can’t be left to the last minute

If you want Adam Accountancy to connect the dots between company profits, shareholder planning, and estate planning, this is exactly the kind of joined-up work we do.

Practical Checklist for 2026 (SME Friendly)

Use this as a working list for tax thresholds 2026.

- Confirm your expected taxable profits (realistic, not optimistic).

- Check whether you have associated companies.

- If you do, recalculate your adjusted £50k/£250k limits.

- Model Corporation Tax at multiple profit levels (e.g., +10%, +20%).

- Confirm whether you might fall into instalment payments.

- Diary the payment deadline (9 months + 1 day).

- Diary the filing deadline (12 months).

- Review owner extraction plan (salary/dividends/pension) with advice.

- Keep evidence for major decisions (bonuses, provisions, capital spend).

- Revisit the plan mid-year—don’t leave it to year-end.

FAQs: UK Corporation Tax Thresholds 2026

What are the UK corporation tax thresholds for 2026?

For FY starting 1 April 2026, the headline structure uses a 19% small profits rate up to £50,000, 25% main rate above £250,000, with Marginal Relief between those figures.

Do I always get the full £50,000 and £250,000 thresholds?

No. If you have associated companies, the limits can be divided across the group, which reduces your thresholds.

Why can the marginal band feel like it’s taxed more than 25%?

Because of the Marginal Relief mechanics, the effective marginal rate in the band is commonly shown as 26.5% for the “slice” of profit in that range.

When do I pay Corporation Tax in the UK?

Most companies (taxable profits up to £1.5m) pay 9 months and 1 day after the end of the accounting period.

When do I file the CT600 return?

The filing deadline is 12 months after the end of the accounting period.

What’s the instalment payments threshold?

HMRC’s “large company” payment regime applies where annual taxable profits are between £1.5m and £20m (with separate “very large” rules beyond that).

Does “tax threshold 2025 to 2026” mean the rates changed?

For many businesses, the bigger change is profit movement and threshold adjustments (e.g., associated companies), rather than headline rate changes. GOV.UK continues to present the same structure as the framework for the period.

How does the inheritance tax threshold freeze implications 2026 relate to me?

If you’re a shareholder-director building wealth in the company, estate and succession planning can interact with company structure, valuations, and reliefs—so it’s worth aligning plans, not treating taxes in isolation.

Final Thoughts: Make 2026 Thresholds Work for You

The right approach to uk corporation tax thresholds in 2026 is not guesswork—it’s forecasting plus structure checks plus good record-keeping.

If you want help modelling scenarios, confirming associated company exposure, or planning around Marginal Relief and payment timing, Adam Accountancy can support you with clear, UK-focused advice. If you’d like, tell me your expected profit range and whether you have more than one company, and I’ll outline the most likely threshold position and planning options for your setup.

To discuss how Accountants in Slough can assist you with your Accounts Preparation, please contact us for a free, no obligation consultation on: 0333 772 1616 or complete our Contact form and we will get back to you.